Phase 3 Outcomes

Relying on wild-caught fish as feed ingredients poses material risks to salmon producers and their investors, and future growth of the salmon farming industry is likely to be constrained if it relies solely on fish-based ingredients and soy protein. Below is a summary of the engagement outcomes. More detail can be found in the Phase 3 progress report, De-risking Salmon Feed: The Wild-Caught Fish Dilemma.

Improvements in disclosures related to feed formulations

Since the start of this engagement, disclosures related to feed formulations have increased overall. All seven companies now disclose the percentage of trimmings used, compared to two doing so in 2020, and four companies reported their share of novel feed ingredients in their latest disclosures, whereas in 2020, none did. However, disclosures of absolute FMFO use in feed are more limited.

90%

of fisheries are overfished or fished at maximum levels.22%

of the world’s total catch of wild fish is processed into fishmeal and fish oil.55%

is the average share of Scope 3 GHG emissions attributed to salmon feed for the companies part of this engagement.25-50%

is the proportion of fish-based ingredients in salmon feed for most engaged companies.6/7

companies have increased the proportion of trimmings in their feed formulations between 2020 and 2024.5/7

companies have increased the absolute volumes of either fishmeal or fish oil used between 2020 and 2024.No target on reducing absolute volumes of wild-caught fish

None of the seven engaged companies have a target to reduce the absolute amount of fish-based ingredients used in feed, despite five of them including production growth targets in their latest disclosures. This leaves doubt as to how these targets will be achieved without a sustainable feed supply. To mitigate their reliance on wild-caught fish, companies have mainly used two strategies – increasing their use of trimmings (i.e. fish by-products) and novel alternative ingredients.

An increased proportion of trimmings is not enough to create sustainable feed

Since the start of this engagement, all companies except Bakkafrost have increased the proportion of marine ingredients derived from trimmings - a key real-world improvement and intended outcome of the engagement.

All companies want to increase their use of fish trimmings; however, it is not clear from their disclosures or the engagement dialogues how much more trimmings are still available. Absolute volumes of FMFO used have increased, and this increase cannot be explained solely by an increased use of trimmings.

Overall, current volumes of trimmings can only take the aquaculture industry so far. Since nearly 90% of wild fish stocks are now fully exploited or overfished, salmon producers cannot rely on trimmings alone to ensure their feed and production models are sustainable.

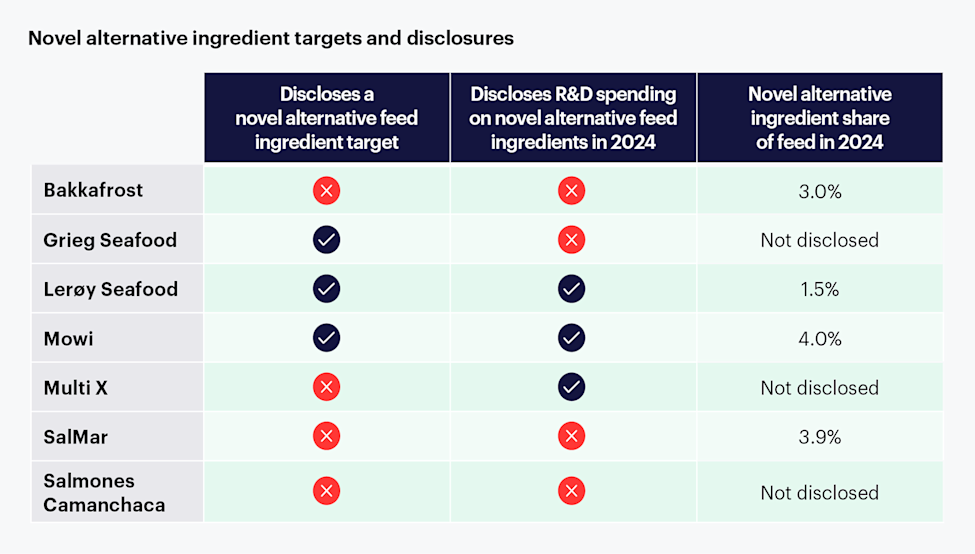

Novel alternative ingredients to FMFO are necessary

The growth of the salmon farming industry is likely to be constrained if the sector solely relies on fish-based ingredients. More first-movers are needed to unlock the potentially pivotal market for alternative ingredients.

FAIRR’s engagement dialogues have revealed that no company has clearly identified alternative ingredients that can replace FMFO at scale, without trade-offs on aspects such as cost, scalability, nutritional quality, carbon footprint or consumer acceptance. Five companies consider algal oil as promising, while four see insect meal as unfavourable.

This lack of consensus from companies creates a muddled market signal, which is likely to slow the transition towards more sustainable feed.

Investors can continue to support company improvements

While this engagement has now come to an end, investors can encourage the salmon aquaculture sector to:

ensure fish availability is considered in companies’ TNFD reporting and risk assessments;

formalise targets on reducing the absolute use of wild-caught fish; and

prioritise research and investment in novel alternative feed ingredients and technologies.

Investors can also help drive a broader transition in the aquaculture industry by:

encouraging companies to include plant-based alternatives in their product portfolios, mirroring what large meat producers have done, and support consumer awareness and market demand for sustainable foods; and

supporting the farming of aquatic species that have a lower environmental impact and do not rely on wild-caught fish feed, such as seaweed, oysters and mussels