Sustainable Aquaculture Engagement Phase 3

Explore the key outcomes from the final year of FAIRR’s Sustainable Aquaculture engagement, which saw seven of the largest salmon producers and 61 investors with US$12.7 trillion in combined assets come together to discuss feed sustainability.

View reportEngagement Overview

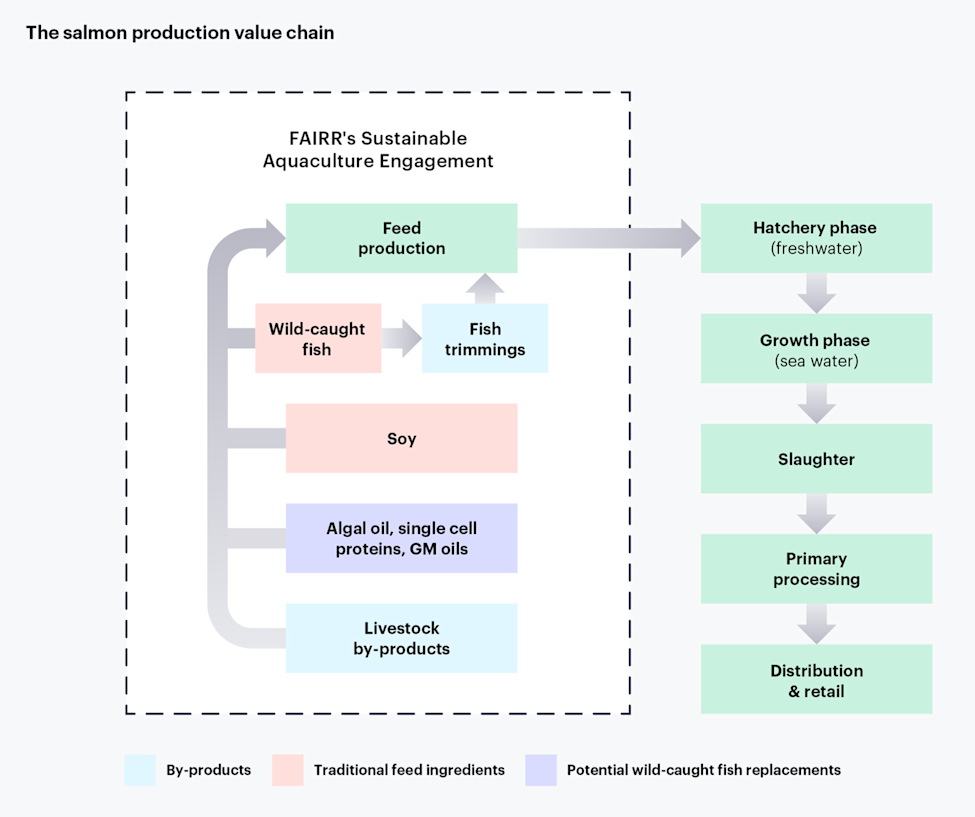

Globally, aquaculture is the fastest-growing food production system, and 70% of salmon are now farmed. Salmon require a high-protein diet, which is commonly derived from fishmeal and fish oil (FMFO) sourced from wild fish, alongside plant-based proteins (such as soy), in their feed. As a result, the industry is acutely exposed to a range of material risks associated with obtaining these ingredients.

While the salmon aquaculture industry’s reliance on wild-caught fish for feed has reduced considerably since the 1980s, the pace of improvement has stagnated since the start of this engagement in 2021.

In 2024/25, FAIRR continued to engage with seven of the largest salmon producers to reduce their reliance on FMFO, mitigate their wider biodiversity risks and identify potential opportunities to adopt novel feed ingredients that can replace FMFO, such as algal oil.

During Phase 3 of the Sustainable Aquaculture engagement, FAIRR held dialogues with all seven companies to discuss their strategies for reducing their reliance on wild-caught fish. Through these dialogues and by analysing companies’ disclosures, FAIRR has found that salmon producers do not have a robust, long-term strategy to further reduce their reliance on wild-caught fish in feed.

Selected Companies

The seven companies selected for this engagement are publicly listed salmon producers with a material share of their respective markets. They are also assessed as part of the Coller FAIRR Protein Producer Index.

Tassal was originally part of this engagement, but since it is no longer publicly listed, it was not included in the Phase 2 and 3 dialogues.

Material Risks

Salmon production and trade has increased significantly in recent decades and is projected to continue growing. Yet the largest producers have generally seen their share price underperform the benchmark over the past five years to April 2025, suggesting investors may see material risks to achieving this promise.

These material risks are linked to feed sourcing. Salmon are a carnivorous species, and the cost and make-up of their feed is a critical part of the farming process. Feed sourcing creates operational risks (fish stock shortages, price volatility), regulatory risks (changes to fishing quotas) and reputational risks (depleting fish stocks that could be otherwise used as food).

By diversifying feed ingredients and moving away from wild-caught fish, salmon producers can help protect their businesses from rising costs, regulatory disruptions and reputational damage, reducing the risks they, and their investors, are exposed to.

Investors Signed On

This engagement is now complete. The final progress report, De-risking Salmon Feed: The Wild-Caught Fish Dilemma, was published in May 2025.