One of the first actions Chile’s newly elected president, Jose Antonio Kast, took after being sworn into office on 11 March 2026 was to become the first sitting premier to attend AquaSur, the region’s largest salmon farming conference.

Kast used the event to highlight his support for the industry, raising the possibility of streamlined permits and reduced bureaucracy as part of a broader deregulation and growth agenda.

This Insight piece highlights how the industry worked hand in hand with regulators to innovate and overcome sustainability-related crises since 2005, and how the largest Chilean salmon producers approach these risks now.

It aims to open a discussion on the value of environmental and health guardrails and whether easing the requirements for new sea cages licenses could bring back past financial risks.

Looking for growth: An overview of the Chilean aquaculture sector

Chile is the world’s second-largest producer of farmed salmon after Norway. Yet, growth of volumes produced stagnated from 2019 to 2024 according to industry figures reported by Multi X. Rekindling growth is therefore a concern for the whole industry.

Six publicly listed companies assessed in the Coller FAIRR Seafood Index operate salmon farms or produce feed for the industry in Chile. European, North American and Asian processors also have exposure to imports of chilean product.

A capital-intensive sector dependent on strong regulatory governance

Salmon farming is more capital intensive than livestock farming because production requires expensive hatcheries, marine cages, specialised vessels, oxygenation and water treatment infrastructure, and long biological production cycles of up to 30 months from birth to slaughter, of which 12 to 16 months are spent in open sea pens.

As a result, the sector relies on reliably high profit margins and predictable operating conditions to generate competitive returns.

Regulation is critical to preserving marine biodiversity as well as the health of the farmed salmon. Until now, this has meant constraining salmon farming expansion, through limitation on stocking density, site zoning frameworks, and biosecurity controls.

In this context, deregulation may reduce costs in the near term, but it also increases exposure to operational volatility and systemic shocks. For investors, the key question is not whether regulation constrains growth, but whether it underpins the resilience required for long-term returns.

Financially material risks amplified by deregulation

Much of Chile’s regulation on farm siting, stocking density, and water quality monitoring emerged in response to disease and pollution crises that have threatened the industry in the past through mass mortalities.

Environmental issues directly impact salmon production volumes

Open‑net salmon farms sit directly in the ocean, so waste (such as uneaten feed, fish waste, antibiotics, and chemicals) flows directly into the surrounding waters. This pollution adds excess nutrients, damages marine ecosystems, and increases the risk of disease and harmful algal blooms, which deplete oxygen and kill fish.

Severe algal blooms linked to El Niño caused major salmon deaths in 2016, 2021, and 2024. 2016 saw 100,000 tonnes of salmon lost to mortality, including 5,000 reported by Multi X. In 2021, Salmones Camanchaca suffered a 26% production volume decline compared to 2020, leading to a US$13 million operating loss, and its peer Mowi recorded a US$12.8 million loss on its Chilean operations.

Against this backdrop, scientists' expectations of a strong, potentially “super” El Niño event in 2026 elevate the likelihood losses linked to significant algal blooms and mortality events.

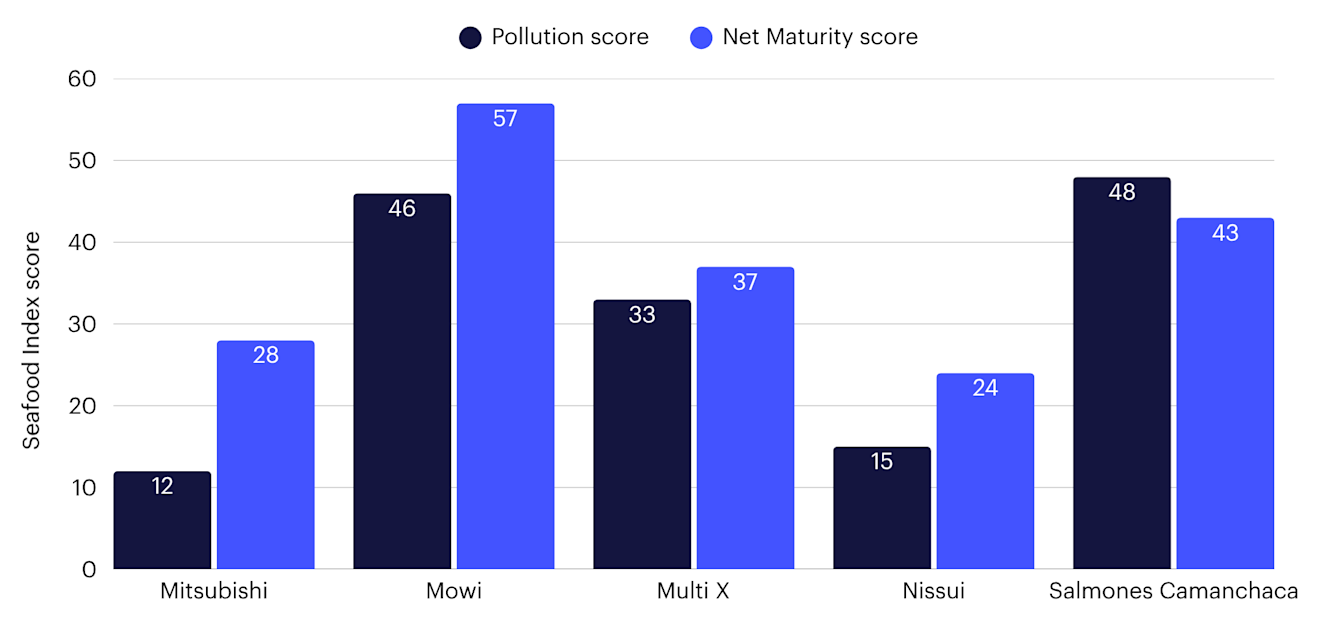

Figure 1: Chilean salmon farm operators score poorly on Pollution on the Seafood Index

Note: The Net Maturity score is an average of all 16 Topic scores in the Seafood Index. Both Net Maturity scores and Topic scores range from 0-100. For more information, please refer to the Seafood Index methodology.

Despite the elevated risks linked to water quality, pollution disclosures related to open-water pen farms are worse than those related to on-land facilities, and no company has reported on water quality indicators or unusual findings from these pens or open-water facilities. This indicates a low level of preparedness to face this issue.

Deregulation that enables higher stocking densities or weaker environmental monitoring could heighten pollution, harm coastal ecosystems and ultimately cause mortality events in salmon farms themselves.

Disease prevails in Chilean salmon farming

In the late 2000s, Chilean production contracted by nearly 75% due to an epidemic of infectious salmon anaemia. The outbreak led to around 25,000 job losses, widespread financial distress and corporate restructures at Multi X and Salmones Camanchaca. As a solution, the Chilean government introduced stricter regulations on stocking densities, sanitary and hygiene protocols to minimise disease and improve medicine effectiveness.

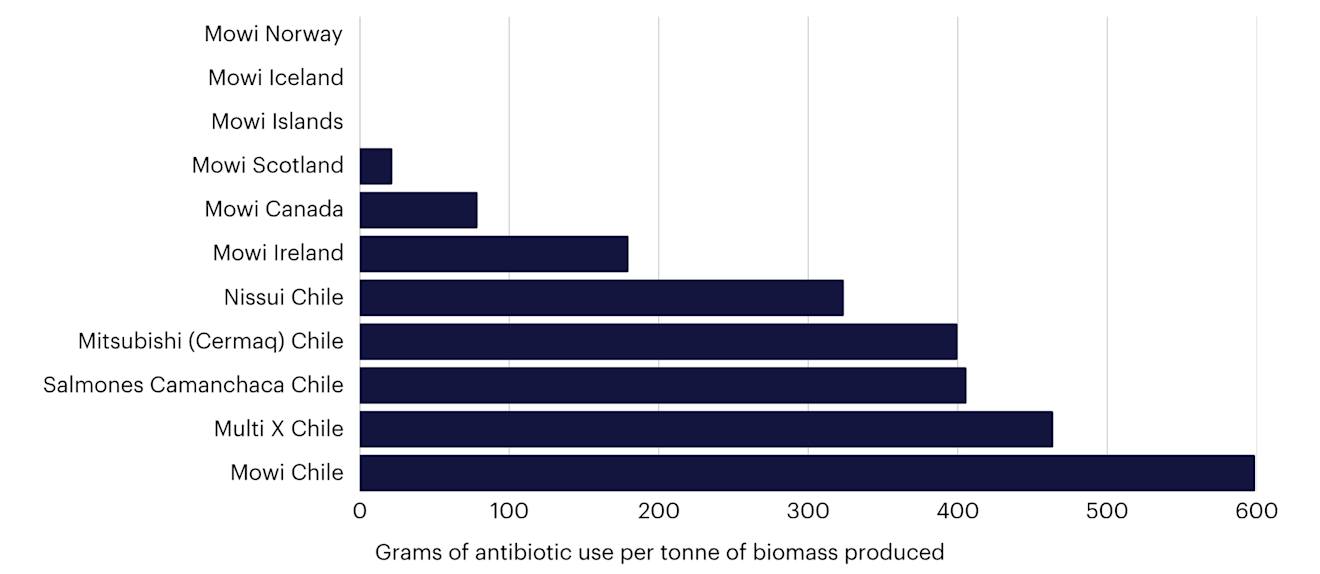

Disease remains a key risk to Chilean salmon production, and antibiotic use is much higher than in other regions (see Figure 2). The reasons for this are complex, but they are tied to salmon not being native to Chile, the prevalence of a disease (salmon rickettsial syndrome) for which there is no effective vaccine, warmer waters and farms being sited closely together.

Figure 2: Active antibiotic use per tonne of biomass produced (g/tonne) using Mowi’s international operations for comparison

Despite the elevated use of antibiotics, infectious diseases remain the leading cause of mortality during the open-water stage of production, forming a particularly acute risk for production in Chile. Companies have invested in antibiotic stewardship and the responsible use of those products. Mowi, Salmones Camanchaca and Multi X score in the top quartile on the Seafood Index on this topic.

Disease-related mortalities and antibiotic use could increase if Chilean regulation mandating relatively low stocking densities of 17kg per cubic metre at the peak of the production cycle, compared to 25kg in Norway, were relaxed.

Fish feed availability and cost depend wild-caught fish scarcity

Feed is the largest expense in salmon farming, representing between 40% to 50% of total costs, and relies heavily on fishmeal and fish oil (FMFO), which are derived from wild-caught fish.

The International Fish Meal and Fish Oil Association reports that the supply of marine raw materials and ingredients that make up FMFO have fluctuated in recent years, driven by changing sea water temperatures and overfishing, as well as resource competition with human and pet uses. FAIRR’s Sustainable Aquaculture Engagement has explored these issues extensively.

This has resulted in cost increases and operational disruptions for salmon producers across the sector, with Chilean companies not immune despite leading peers in reducing FMFO dependency to below 5% of formulation by including micro-nutrients and other animal proteins.

In 2023 and 2024, fish oil prices reached US$7,200 per tonne after Peru, the world’s largest FMFO producer and exporter, cancelled its anchoveta fishing season due to low stocks driven in part by strong El Niño events. Limitations on feed ingredient availability act as a growth constraint to the sector regardless of regulation.

Overall, the aquaculture sector remains relatively immature in its management of risks associated with the marine ingredient sustainability, and Chilean companies score low on this topic (38/100 on average) on FAIRR’s Seafood Index.

Environmental limits, not regulation, constrain industry

A central assumption underpinning deregulation is that reducing regulatory burden will unlock growth. However, in Chilean salmon aquaculture, growth is ultimately constrained not by policy, but by environmental limits.

Attempts to push production beyond these limits have historically resulted in materially financial risks via disease outbreaks, environmental degradation and, ultimately, regulatory tightening. Chile’s experience—including past crises linked to overexpansion—demonstrates that unmanaged growth can destroy rather than create value.

By taking a proactive approach, investors can help ensure that short-term policy shifts do not compromise long-term value creation.

Learn more about the Coller FAIRR Seafood Index.

FAIRR insights are written by FAIRR team members and occasionally co-authored with guest contributors. The authors write in their individual capacity and do not necessarily represent the FAIRR view.

Written by

Manager, Research & Engagements - Oceans

Head of Nature Programmes

Senior Investor Outreach Manager